How much income do you need to buy a house?

Home buyers need to meet certain standards to get a mortgage. There are minimum credit scores, employment requirements, and more. But many first-time home buyers don’t realize that there’s actually no minimum income required to buy a house.

Instead, you must earn enough to qualify for the requested loan amount. And the money you earn must be an acceptable type of income (though most types are perfectly fine). Here’s how to determine if your income will qualify for a mortgage.

Income requirements to buy a house: Key takeaways

Home buyers at any income level can apply for a mortgage. The most important thing isn’t how much money you earn, but rather, that your income meets a few key requirements.

Income requirements for a mortgage:

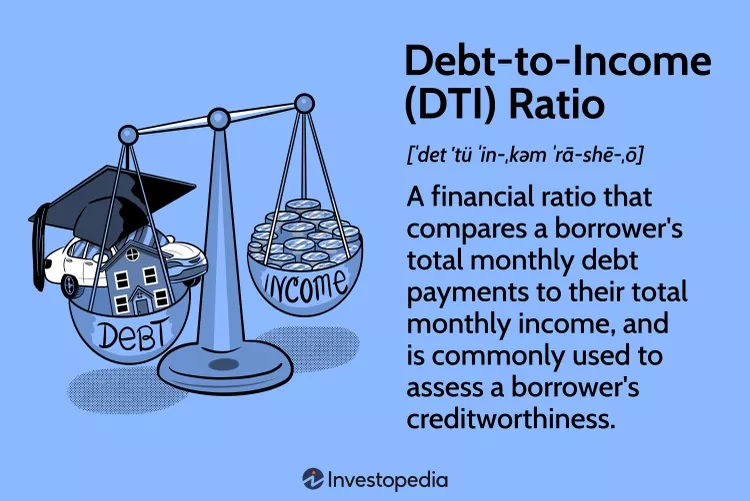

- You need a reasonable debt-to-income ratio — usually 43% or less

- You must have been earning a steady income for at least two years

- Your income must be expected to continue for at least three years

Outside of those basic criteria, income requirements for a home loan are flexible. Most types of income can qualify — from standard salaries to the commission, investment, self-employment, bonus, and RSU income.

Thanks to today’s flexible mortgage programs, you don’t need a high salary to buy a home. Low-income mortgage programs can make buying affordable even for families without a lot of cash flow or savings.

Mortgage income requirements in 2023

There’s no true “minimum” income requirement to buy a house. Lenders just want to know if you can afford the mortgage. That means you need to prove you have enough income to cover your future monthly payments.

One way lenders determine affordability is by looking at your debt-to-income ratio (DTI). DTI compares your existing monthly debts with your monthly income. This shows how much money you have “leftover” each month for a mortgage payment.

Your annual income must be reliable and stable, too. After all, most mortgage loans last 30 years. So you need to have a steady cash flow and the ability to keep making loan payments over that time.

Most home loan programs require two years of consecutive employment or consistent income, either with the same employer or within the same field. This is a sign of stability, indicating that your annual income will likely remain reliable for at least three years after closing on your home purchase.

There are exceptions to the two-year income rule, though. For example, “If you are in a profession like a nurse or a lawyer and you recently graduated, schooling will count towards this 2-year requirement,” says Jon Meyer, The Mortgage Reports loan expert and licensed MLO.

What sources of income qualify for a mortgage?

Mortgage lenders can approve borrowers with all sorts of income, such as salaried employees, hourly wage earners, freelancers, business owners, and those who receive Social Security payments. But any source of income must meet certain guidelines to qualify on a mortgage application.

Employees (salaried/hourly wage)

Employees can use the income they receive from a salary, hourly wage, commissions, or overtime, as well as restricted stock unit income and bonuses for mortgage-qualifying purposes. You must provide your lender with your most recent paycheck stubs, W-2s, and tax returns from the previous two years. Annual income must be consistent over this two-year period.

To use commissions, overtime, restricted stock unit income, or bonus income for qualifying purposes, you must show evidence of this income continuing for at least two to three years post-closing. This involves your employer providing written confirmation.

Freelancers and self-employed

Getting a mortgage as a self-employed person — which includes independent contractors, freelancers, gig workers, and business owners — is a bit trickier. But it’s not impossible by any means.

Self-employment income can fluctuate from year to year. Not only will you provide your complete tax returns from the previous two years, but your annual income must either remain the same or increase during these two years.

A minor decrease from one year to the next is usually okay. Just know that lenders typically average your self-employment income over this two-year period to determine your qualifying amount. So if your freelance income is $40,000 one year and $75,000 the next year, your lender uses an income of $57,000 to decide affordability.

As a self-employed borrower, be mindful that too many business deductions on your tax return can reduce your qualifying amount. Lenders use your net income after deductions for qualifying purposes. They can add back some deductions, such as those for mileage and use of a home office. As a rule of thumb, the more business deductions you have, the less you earn on paper.

Other types of income that count toward mortgage qualifying

Here’s what you need to know when using other sources of income to qualify for a home loan:

- Dividend income: This income must be regular, and you must show a two-year history of receiving dividends

- Retirement income: Income must continue for at least three years post-closing

- Social Security income: This income must continue for at least three years post-closing

- Alimony and child support: You must have received regular payments for at least six to 12 months prior to getting the mortgage, and support payments must continue for at least three years post-closing. You’ll need to provide a copy of a divorce decree and other court orders

If you’re not sure whether your income qualifies, talk to a mortgage lender. Your loan officer can help you understand which sources of income are eligible and the home prices you can afford based on your monthly cash flow.

Source: themortgagereports.com